Are You Getting Value from Your Value Index?

Value has been one of the most studied investment factors since Benjamin Graham introduced it in the 1930s. For decades, the value premium has been treated as a core building block of smart beta and a reliable source of long-term return.

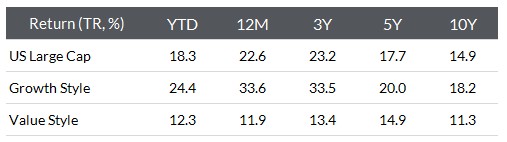

But the last decade hasn’t looked like a victory lap for value. When viewed through the lens of style indexation, value has delivered disappointing returns relative to cap-weighted indexes, while growth - boosted by AI enthusiasm and the dominance of the Magnificent Seven - has dominated performance. As Figure 1 shows, the gap hasn’t just persisted; it has widened.

Figure 1: Performance of US Large Cap, Value and Growth Styles

Source: Wilshire Indexes. Performance data as of October 31, 2025.

It’s no surprise many investors have concluded that value simply “stopped working.”

That conclusion is wrong.

The issue isn’t Value – it’s how Value is packaged

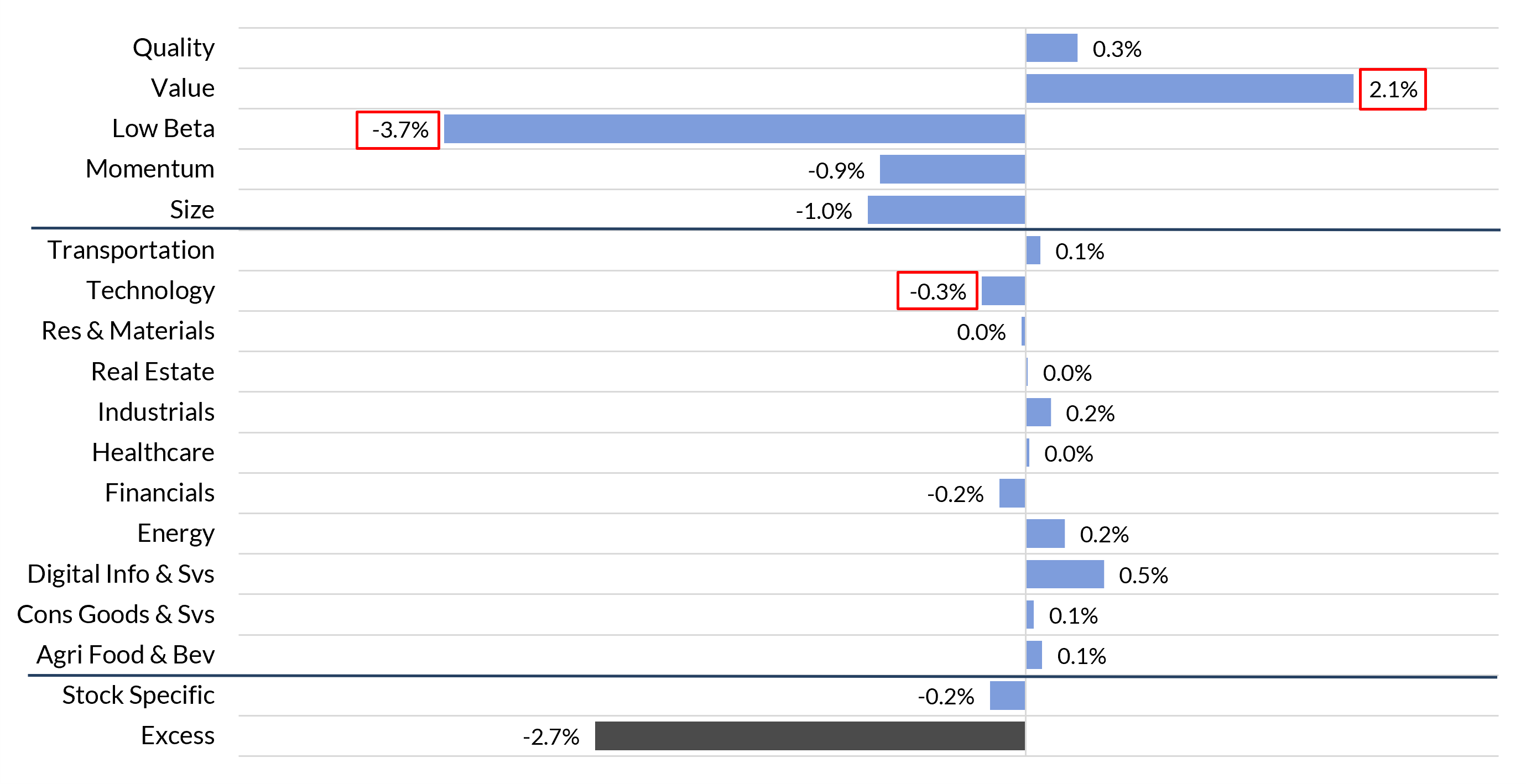

To understand what really happened, we decomposed the performance of the Value Style index over the last five years (Figure 2).

Figure 2: Five Year Performance Attribution of Value Style

Source: Wilshire Indexes. Attribution data between October 31, 2020 and October 31, 2025.

The result is straightforward:

- The value factor contributed greater than 2%p.a. to the performance of Value Style over the last 5 years

- The net drag came from other factor and industry exposures embedded in the index, notably from the low beta factor and technology sector

In other words, the disappointing headline results were not driven by the value factor itself. They were driven by the combination of non-value factor and industry exposures that came along for the ride.

Those effects accumulated over time - not because value failed, but because Value Style bundles value together with a set of additional exposures investors did not explicitly ask for.

Pure Value Versus Value Style

Wouldn’t a better way to capture value be to use an index that neutralizes these off-target contributions and whose performance better aligns with the value premium?

That is exactly what the Pure Value Index delivers.

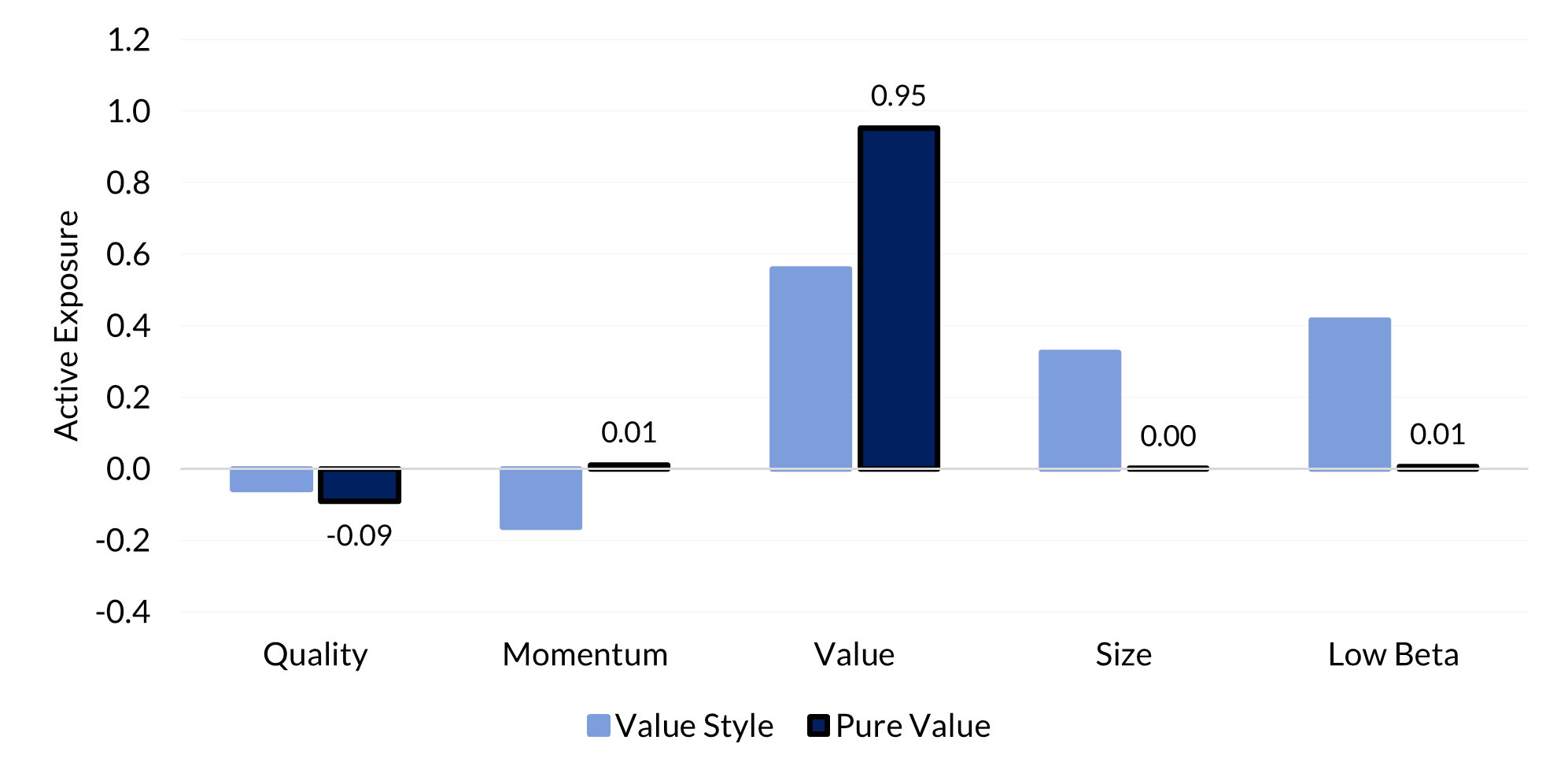

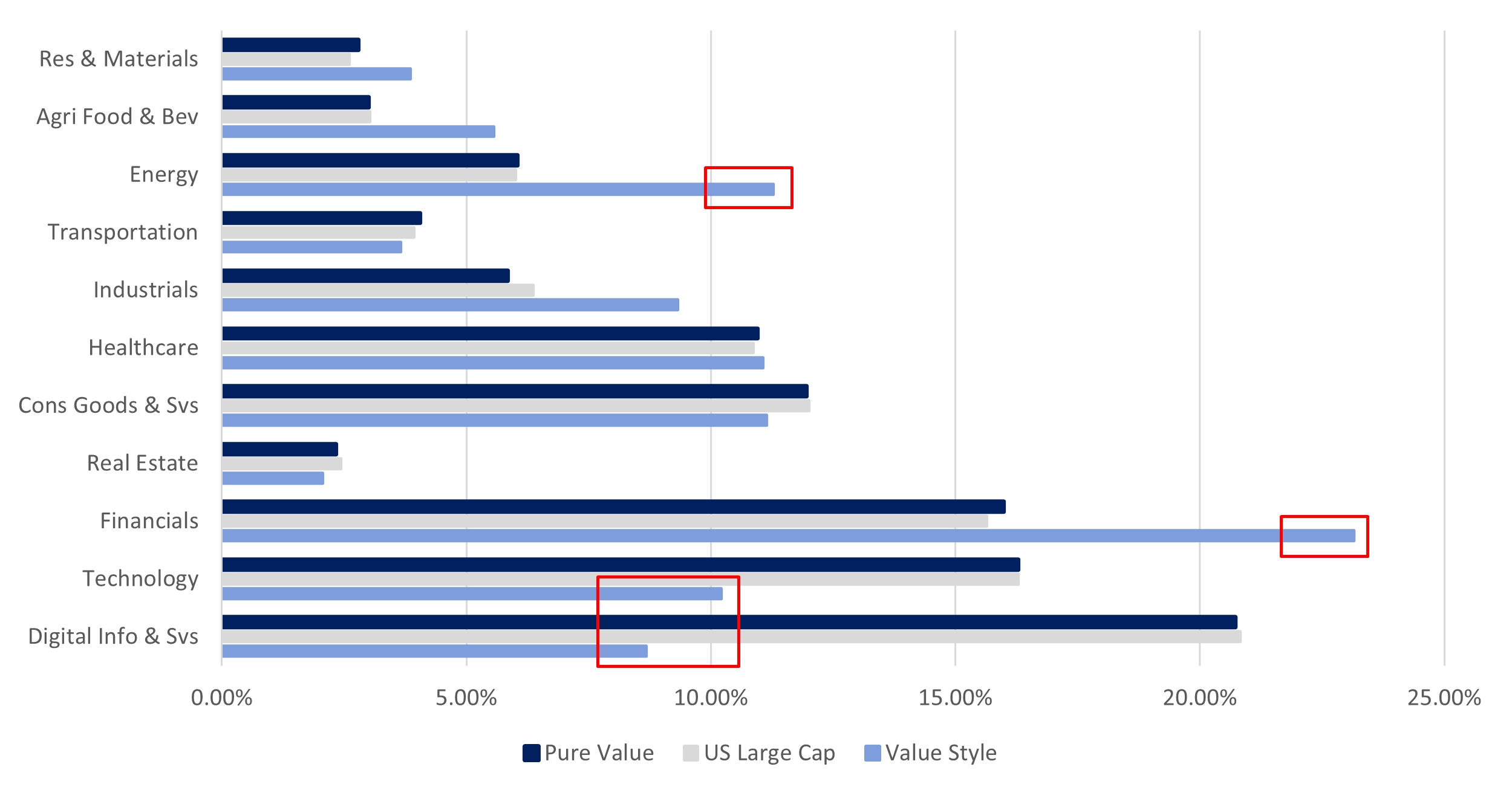

The Pure Value Index removes these additional influences and aligns industry weights with the broader US Large Cap universe. Figures 3 and 4 highlight the differences:

Figure 3: Five Year Average Active Factor Exposures: Pure Value vs Value Style

(Standard deviation from US Large Cap level)

Source: Wilshire Indexes. Averages between October 31, 2020 and October 31, 2025.

Figure 4: Five Year Average Industry Weights: US Large Cap vs Value Style vs Pure Value

Source: Wilshire Indexes. Averages between October 31, 2020 and October 31, 2025.

Note that:

- Pure Value minimizes non-value factor exposures, including the low-beta tilt that hurt Value Style’s five-year performance

- Its industry weights match the market, avoiding the persistent underweight to Technology seen in Value Style

The result is an index that reflects value, not value combined with other factor and industry effects

What happens to Performance when you remove the distortions?

Once those additional exposures are reduced, the performance profile changes. Over the past five years (Figure 5),

Figure 5: Five Year Performance: US Large Cap, Growth Style, Value Style and Pure Value

.svg)

Source: Wilshire Indexes. Data as of October 31, 2025.

Pure Value outperformed Value Style, the US Large Cap benchmark, and even outperformed Growth Style!

The story is not that value “failed”

It’s that the way value has been implemented in traditional style indexes turned a positive factor contribution into a disappointing overall outcome.

Why This Matters for Investors

Most investors rightly assume that their value index gives them value exposure.

But it's likely that it also gives them other embedded exposures that can dilute or even reverse the effect they are trying to capture.

The five-year outperformance of the Pure Value Index directly challenges the narrative that “value hasn’t worked”.

Value has been working just fine. Any disappointing results arise from the construction of value indexes, not from value itself.